Let me start you out with something mind-blowing.

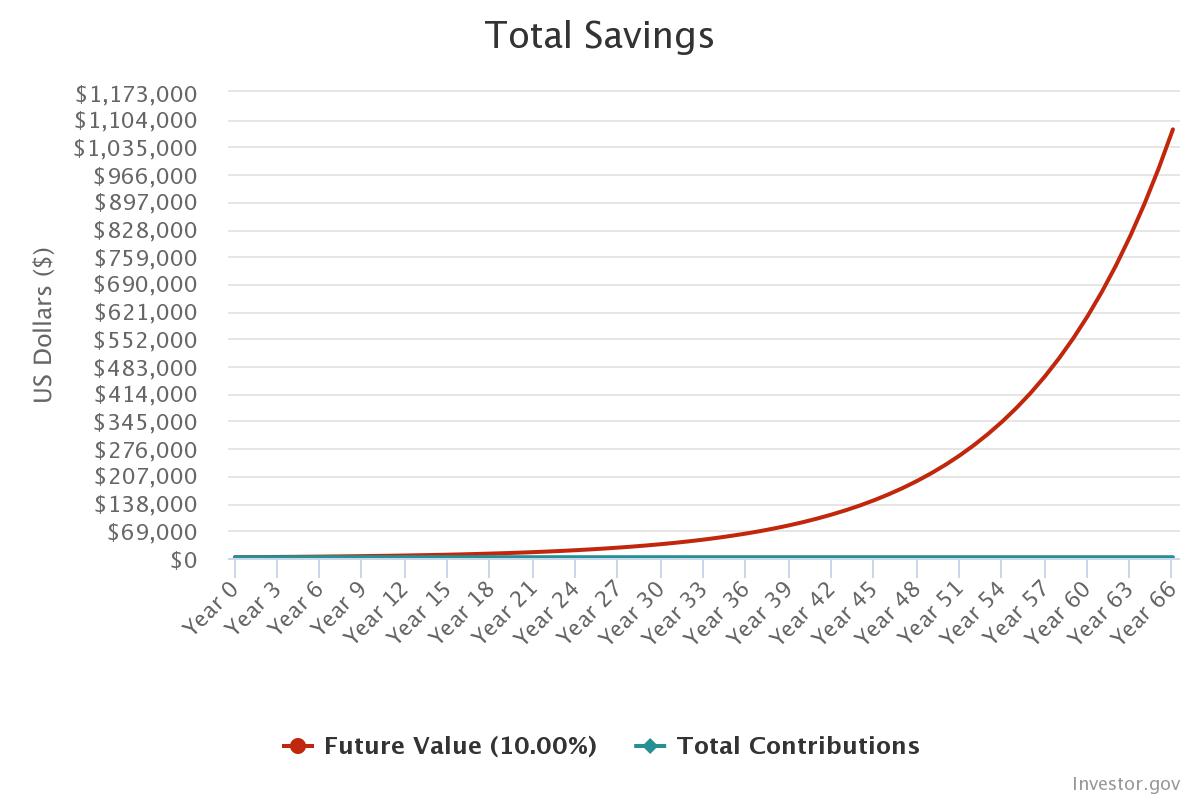

If your parents would have invested $2,000 at your birth into the S&P 500 and never did anything else, you'd likely have a million dollars when you retired (age 66, to be exact).

Can you become a millionaire just by investing $2,000 one time?

Seriously. Just a $2,000 one-time investment at an average rate of return of about 10%. That's it.

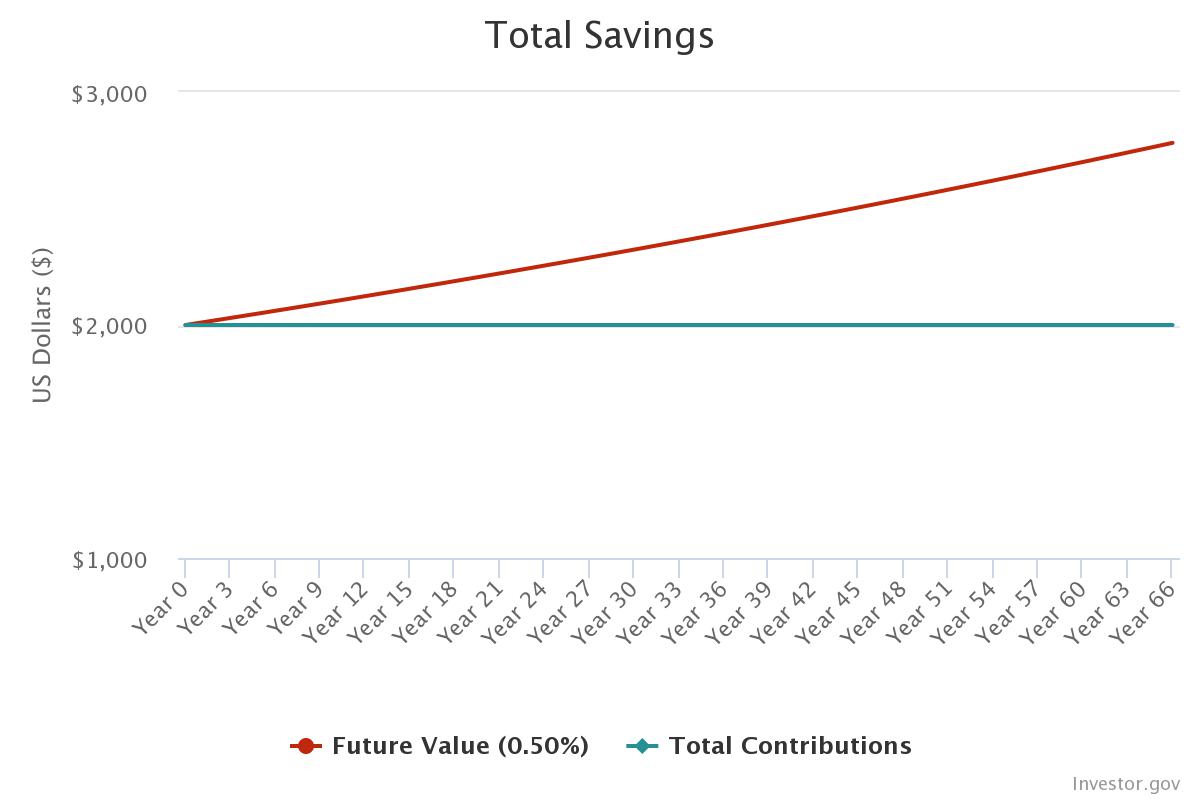

Now let's look at what would happen if your parents had just put that $2k at your birth into a savings account and let it ride until you retire.

And once you factor in inflation, that $2,000 saved would be worth next to nothing by retirement.

The point is simple: saving at today's interest rates is actually going backward with your money. It's better than wasting it, but if you really want to move forward, investing wisely for the long term has proven to be the most reliable way to do it.

In this guide we'll break it down — the surprisingly simple math behind a million-dollar nest egg, how to find the money to invest in the first place, and the one investing formula the world's greatest investor recommended to his own widow.

Quick note: I'm a financial educator, not your financial advisor. Take this as financial education and not specific advice for your situation — deal?

But should a Christian even want this?

Before we get into the math, let me address something — because for a lot of us this is the real hesitation: is it even okay to want to build wealth?

I wrestled with this for years. There are verses that can make you nervous about money, and it held me back for a long time. But then I started digging through the Bible, and I saw so many wealthy men and women of God who didn't serve money, but who wanted to serve God with money. And that is what we're after.

It comes down to heart posture. John Wesley lived by a simple rule:

Earn all you can.

Save all you can.

Give all you can.

He didn't want riches for himself. He wanted to impact the world more with what he'd been entrusted with.

That's the whole point of this for us too. It's not about building the biggest net worth possible and counting our dollars like Scrooge McDuck. It's about this: how can we multiply what we've been entrusted with, be good stewards of it, and do more for God's kingdom?

Let me tell you where this got real for Linda and me.

We were at a conference, and a woman was sharing her story of discovering human trafficking. She described a five-year-old girl locked in a cage a few stories up in a small town overseas. She asked her guide why that little girl was up there, and he said:

"Because she's not broken yet."

The cost of inaction

Linda and I both sat there and started bawling. And in that moment the money stuff became less important and more important at the same time. Less important as a number. More important as a tool. Because I believe that little girl is crying out to God for help — and the truth is, we are God's answer to those prayers. Every dollar we steward well can help rescue children like her.

That is why learning to build wealth God's way matters so much. Not so we can have more. So we can do more.

So let's build wealth — but let's do it for the right reasons.

Sound good?

First — let's talk about saving a million bucks.

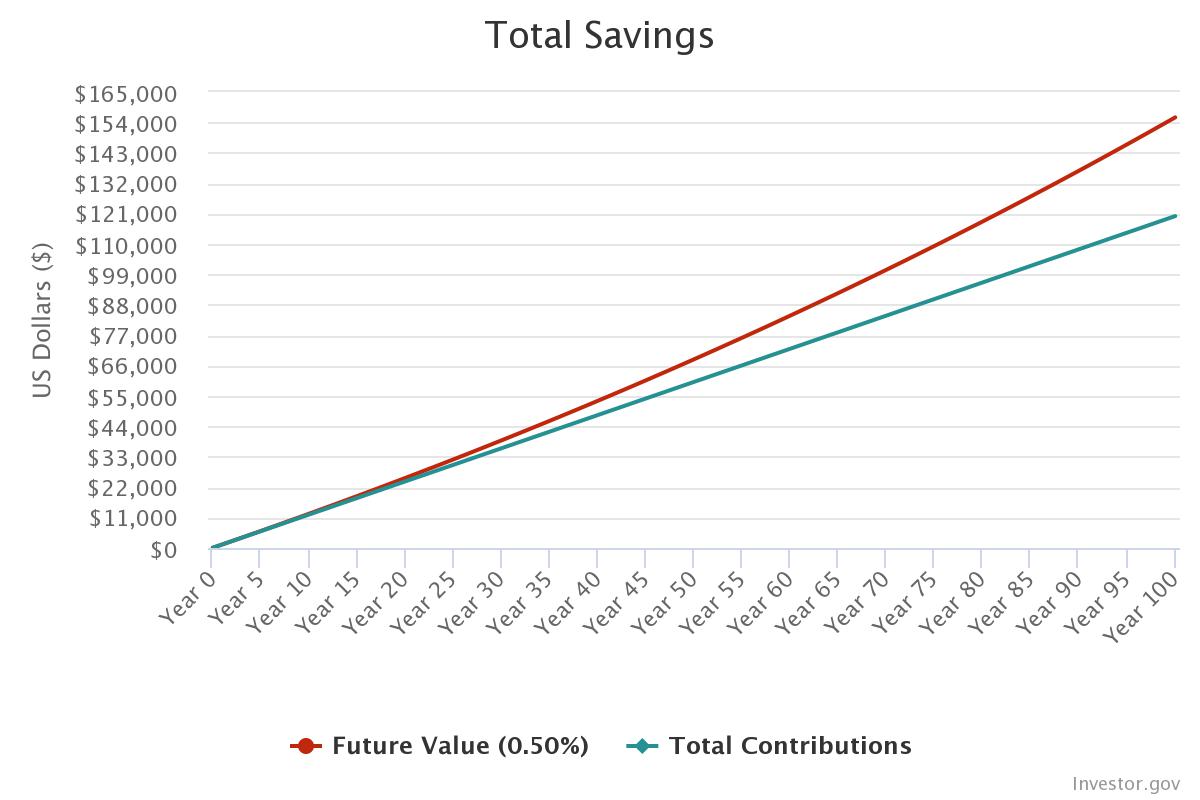

Trust me, you don't want to try to save a million bucks.

Even if you saved $100/month for the next 100 years at today's interest rates, you'd end up with about $156,000.

Pretty much no one is going to save their way to a million. You need to invest it.

Now — the shorter path.

The S&P 500 has averaged about 10% per year for the last 100 years. Of course nobody knows the future, but that's a better track record than anything else we have to guess at.

Assuming that 10% average continues and you contribute $500/month ($6k a year) to an S&P 500 ETF like VOO, here's what we could expect to see:

How much do I need to invest to become a millionaire?

Same assumed average return, just from another angle — here's how the monthly contribution changes the time it takes to reach $1M.

- $100 / month45 yrs to $1M

- $300 / month34 yrs to $1M

- $500 / month29 yrs to $1M

- $1,000 / month23 yrs to $1M

The good news: anyone can do this. You don't need a financial advisor. You don't need to be a financial expert. You don't need to spend hours every day researching stocks or crypto. It's far easier than the financial industry wants us to believe.

Finding some money to invest.

This is the one I hear most: "I don't have an extra $500 a month. I don't even have $100."

Let's fix that. Because here's the reframe that matters: you don't need a spare $1,000. You need to free up your first $100. And it can start even smaller than that — as little as $5. The idea that you need a big pile of money to begin is just a lie that keeps people on the sidelines for years. You don't need a lot to start. You need to start.

And remember the math from earlier: even $100 a month, given enough time, turns into a million dollars. Small and consistent beats big and someday, every single time.

So let's find that first $100. There are really only two options.

Cut and free up expenses.

My millionaire mentor taught me there are two key areas where Americans waste most of their money:

- Cars. From the purchase to maintenance, gas, and insurance.

- Eating out. Switch to every other day and you can realistically save $200–$500/month.

Earn a little more.

A small side hustle a few hours a week is all it takes:

- Deliver for DoorDash a few hours each weekend (~$15–$20/hr).

- Run Facebook ads for local businesses.

- Pet sit through Rover — literally get paid to play with a dog.

"Whoever gathers money little by little makes it grow."

That's the whole strategy. Small, faithful steps, done consistently. You don't have to start big. You just have to start.

Turning that extra cash into a million bucks.

I spent the first 10 years of my career working at a bank and investment services company. There's basically a conspiracy in the financial industry to make successful investing far more complicated than it needs to be.

The truth: it's actually ridiculously easy to succeed as an investor — if you can just be consistent and patient.

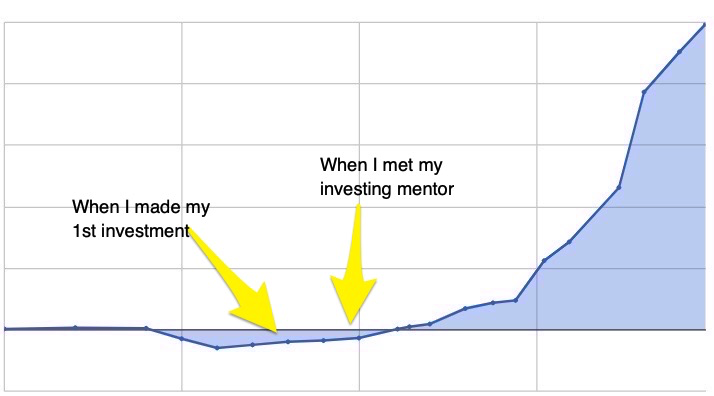

I still remember getting started on this journey, hearing this same advice, and hoping it was true. Honestly? I wasn't sure. I just trusted my mentor and a few of the great investing books I'd read.

Now, 16 years in — having generally stayed consistent and patient — I can say with confidence that this simple process works. Here's a look at how our assets have grown since I first learned this from my mentor:

What's the catch?

There is one. It's called risk.

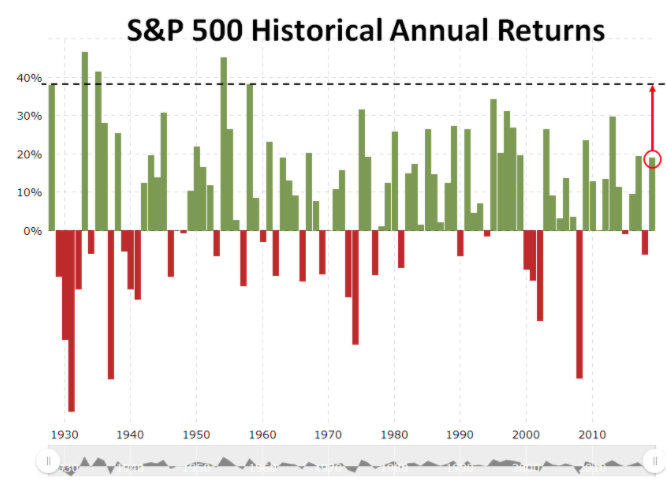

Investing in anything can lose money. If you invest in the S&P 500 you will have years where you lose money. Just look at how many red years there are on this chart:

So let me not gloss over this, because it's the thing that stops most people. Here's the part that changed how I look at it: the longer you stay in, the less likely you are to lose.

If you'd been invested in the S&P 500 for just one year, the worst you could have done historically is about a -40% year. That's the number people are scared of. But watch what happens as you give it time:

- Hold for 1 yearworst case ≈ -40%

- Hold for 3 yearsworst case ≈ -17%

- Hold for 5 yearsworst case ≈ -6 to -7%

- Hold for 10 yearssmaller still

- Hold for 15 yearsnever a loss, historically

- Hold for 20 yearsworst case still ≈ +6–7%/yr

Bar = size of the worst historical drawdown

Read that again. In the entire history of the S&P 500, there has never been a 15-year stretch where you'd have ended up with less than you put in. The longer you hold, the less likely you are to be down. So time isn't just how the money grows. Time is how the risk shrinks.

Here's a recent example. In spring of 2020 the S&P dropped about 34% in a few weeks. People panicked and sold. By the end of that same year it had fully recovered and then some. The job is simply to stay in your seat.

Now flip it around. A savings account feels safe, because you never watch the number drop. But is it really? Right now you're quietly losing several percent every single year to inflation. The number on the screen stays the same while the value underneath it shrinks. A slow, invisible loss instead of a visible one — and over a few decades, the more dangerous one.

So yes, investing carries risk. But doing nothing carries a cost too — one you feel, and one you don't. Given enough time, the market has been the most reliable way we know to come out ahead.

The world's greatest investor's greatest advice.

You know Warren Buffett. I talk about him all the time — and for good reason. He's the greatest investor of the last 100 years and at this point is just a really wise old man.

His company, Berkshire Hathaway, is basically a mutual fund. Since Warren took it over in 1964, it has averaged about a 20% annual return. Simply amazing.

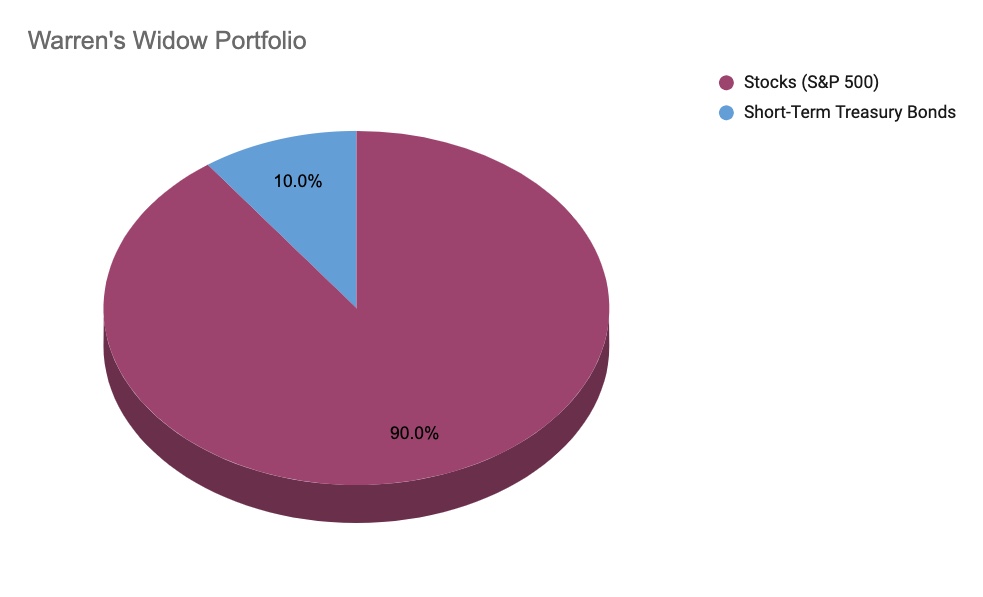

At one point Warren shared the exact instructions he left his wife for how she should invest after he's gone. What investing advice do you think the world's best investor gave his own widow?

My mind was blown when I read what he wrote.

"Put 10% of the cash in short-term government bonds and 90% in a very low-cost S&P 500 index fund. (I suggest Vanguard's.) I believe the trust's long-term results from this policy will be superior to those attained by most investors…"

That's it. The simplicity is mind-blowing.

Buffett continued: "I laid out what I thought the average person who is not an expert on stocks should do… She'll do fine with that. And anybody will do fine with that. It's low-cost, it's in a bunch of wonderful businesses, and it takes care of itself."

If you're curious, here are Vanguard's ETFs for each:

- 90% Vanguard S&P 500 ETF (VOO)

- 10% Vanguard Short-Term Treasury ETF (VGSH)

It really can be this simple.

As Billionaire investor George Soros says:

"If investing is entertaining, if you're having fun, you're probably not making any money. Good investing is boring."

If you take nothing else from this, but start automatically doing the one thing Warren recommended to his widow (ideally in a Roth IRA so you don't have to pay taxes when you cash out), when you look back 20 or 30 years from now I think your mind will be blown.

16 years in, that's certainly been the case for me. Don't underestimate the simplicity of it.

The most important key nobody talks about.

Time.

If you've been paying attention, time is the real factor here. That's why a single $2,000 investment can turn into $1M — because it takes 65 years. And if you want to hit $1M in 23 years, you need to invest $1k per month. Less time, more money.

There's something almost built-in about this. From the very start, God designed things to grow slowly and multiply in their season. Seedtime, then harvest. Our part is to plant and stay patient.

But the great thing is that time does the heavy lifting for us — if we let it.